Ghost Distilleries: The Vanished Names That Haunt the Whisky Market

There is a particular kind of reverence reserved for whisky from distilleries that no longer exist. In an industry built on time, patience, and provenance, the bottles that bear the names of silent stills occupy a category of their own. Collectors call them ghosts. The trade calls them closed, mothballed, or demolished. Whatever the terminology, the economic and emotional gravity is the same. Once the warehouses empty, no more will ever be made.

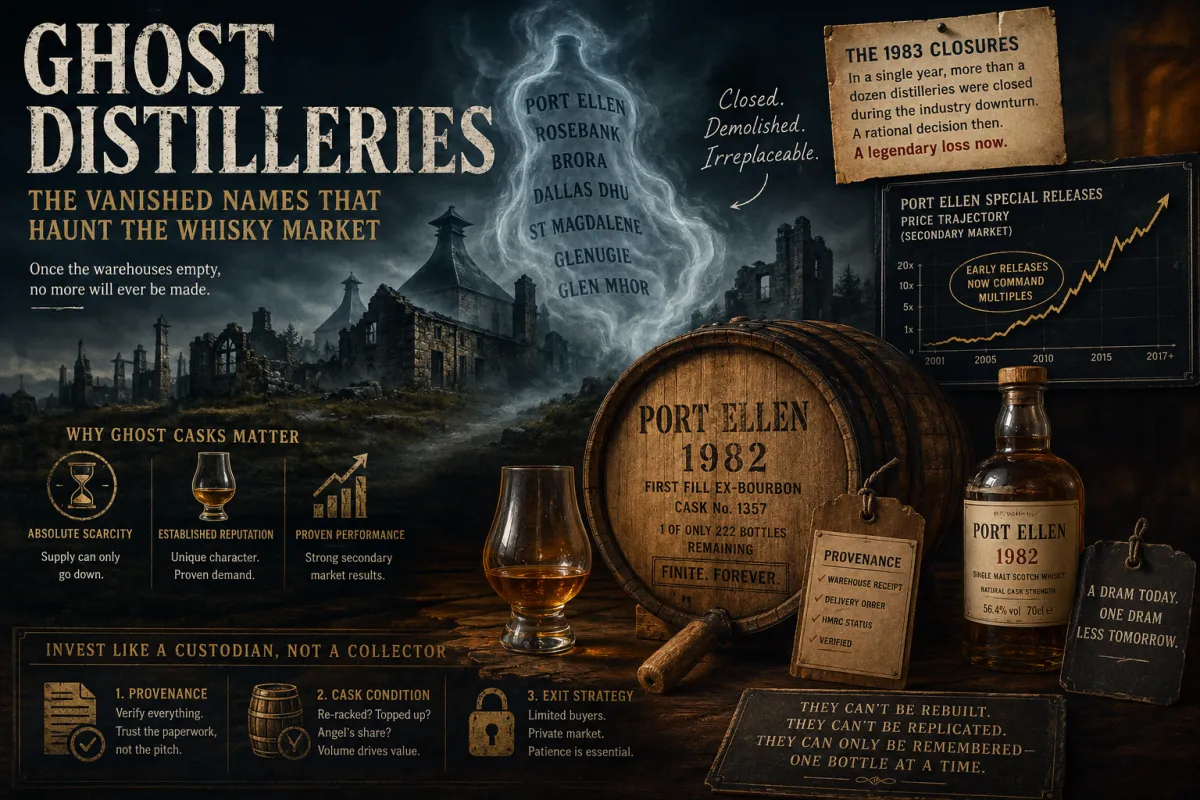

The term ghost distillery refers to a Scotch whisky distillery that has ceased production permanently, with the site dismantled, repurposed, or demolished such that revival is no longer feasible. This distinction matters. Brora and Port Ellen, both shuttered in 1983, were ghosts in spirit for nearly forty years before Diageo announced their resurrection. Their reopening reminded the market that the line between dormant and dead is not always fixed, but the casks distilled before closure remain finite, irreplaceable, and uniquely valuable. The new make spirit from a revived distillery, however faithful the recreation, is not the same liquid as what slept in oak through the decades when the lights were off.

The wave of closures that defined the ghost distillery phenomenon came in the early 1980s. The whisky loch, a period of severe overproduction running into the late 1970s, collided with collapsing global demand. The Distillers Company Limited, predecessor to Diageo, made the commercial decision to close more than a dozen distilleries in 1983 alone. Among the casualties were Port Ellen on Islay, Brora in the Northern Highlands, Rosebank in the Lowlands, Dallas Dhu in Speyside, Glenugie in the eastern Highlands, Glen Mhor in Inverness, and St Magdalene in Linlithgow. Each closure was a rational response to a glutted market. Each, in hindsight, removed a unique character of Scotch from the world forever.

The investment case for ghost distillery casks rests on three pillars: absolute scarcity, established critical reputation, and demonstrated secondary market performance. Unlike rare casks from operating distilleries, where future releases continue to set reference prices, ghost stock can only diminish. Every bottling reduces the remaining inventory. Every dram poured is a small, irreversible subtraction. Port Ellen, in particular, has built a reputation for heavily peated Islay spirit with a coastal complexity that aficionados argue cannot be replicated. The annual Diageo Special Releases featuring Port Ellen between 2001 and 2017 produced a clear price trajectory, with early releases now commanding multiples of their original retail value at auction.

Rosebank presents a parallel case in the Lowlands, prized for its triple-distilled, grassy, floral profile. Brora, with its waxy, lightly peated Northern Highland character, has drawn comparisons to old-style Clynelish. Dallas Dhu, preserved as a museum by Historic Environment Scotland, last distilled in 1983 and represents perhaps the cleanest example of a true ghost, with the site itself frozen in time. Casks from these names rarely surface in the open market. When they do, the transactions tend to be private, relationship-driven, and priced accordingly.

For investors considering exposure to ghost distillery stock, several factors warrant disciplined assessment. Provenance documentation is paramount. The further back a cask was distilled, the more important the chain of custody becomes. Warehouse receipts, delivery orders, and HMRC duty status must be verified through the bonded warehouse rather than accepted on a broker's word. Cask condition is the second consideration. Liquid that has been in oak for forty years has likely been re-racked, topped up, or rejuvenated at various points. Each intervention has implications for the final character and the bottling yield. Angel's share losses on long-matured casks can be considerable, and the remaining volume directly determines economic outcome at exit. The third consideration is exit strategy. Ghost casks are not liquid in the financial sense. Buyers exist, but they are few, and the marketing process typically requires patience and discretion.

Pricing is where romance meets arithmetic. A first-fill ex-bourbon Port Ellen cask from the early 1980s, if one were to surface, would not be priced on a CAGR model alone. Independent bottlings of Port Ellen single casks have crossed five-figure sums per bottle at auction, and the cask-level mathematics follow accordingly. Whether such pricing represents fair value depends entirely on the holding period and the buyer's view of where the rare whisky market settles over the next decade. The market has corrected before. It will correct again. But the supply side of ghost distillery stock has only one direction.

Ghost distilleries occupy the apex of Scotch whisky investment for reasons that are structural rather than sentimental. They cannot be diluted by new production, repositioned by marketing, or expanded by capacity investment. They are, quite simply, finished. For the disciplined investor, that finality is the entire point.

By Alexander Knight